IIP-171: Launch the Diversified Staked ETH Index (dsETH)

IIP: 171

Title: Launch the Diversified Staked ETH Index (dsETH)

Status: Proposed

Author(s): @allan.g (On behalf of the Index Coop Product Team)

Reviewed by: @edwardk @DevOnDeFi @afromac

Created: 22 December 2022

Quorum: 479,004 (10% of Votable Supply)

1.0 Simple Summary

The Product team would like to propose that the Index Coop launch the Diversified Staked ETH Index (dsETH), which will provide diversified exposure to the top liquid staking tokens in the Ethereum ecosystem.

2.0 Abstract

dsETH will enable token holders to access the best ETH liquid staking tokens through a single token, using a methodology that promotes decentralization and competition amongst provider protocols. dsETH will also be the first Index Coop product built on Index Protocol, a good-faith fork of Set Protocol v2 that is owned and operated by the DAO.

2.1 Motivation

At the time of writing, there is nearly $8B worth of ETH in liquid staking pools, representing almost a third of all ETH staked. Lido’s stETH product commands the majority of the liquid staking market, but protocols like Rocket Pool and Stakewise have emerged as competitors. As a result, users seeking to stake their ETH today must consider a variety of value propositions, principles, and protocols.

With dsETH, users can instantaneously distribute their stake across the top liquid staking protocols and earn an aggregate staking return. Rather than selecting a single liquid staking token and concentrating risk, dsETH token holders benefit from its innate diversification - both at the asset and the issuing protocol layer. The dsETH methodology is also weighted towards protocols with more node operators and balanced distribution of stake, with the objective of encouraging decentralization and competition in the on-chain liquid staking market.

2.2 Rationale

ETH is the most prominent and liquid asset in DeFi. It functions as a utility token, a medium of exchange, an interest-bearing asset, and a store of value (amongst other things). With a market cap of $146B and an average annual return of 194% over the last five years, there are many investors eager to grow their ETH holdings.

Staking is one of the most popular methods for earning a return on ETH and it is often referred to as the risk-free rate within the Ethereum ecosystem. Dozens of different “staking-as-a-service” providers have emerged as a result, ranging from centralized entities like Coinbase and Kraken to decentralized protocols like Lido and Rocket Pool.

Within the DeFi ecosystem, protocols that offer liquid staking tokens - interest bearing tokens that represent staked ETH and its rewards - have experienced tremendous growth due to low deposit requirements and higher returns compared to centralized services. The largest decentralized protocols are also incentivized to maximize transparency and minimize trust assumptions for users, and also provide secondary market liquidity for their liquid staking tokens.

As more liquid staking protocols emerge, stakers are confronted with the decision of which one(s) to entrust with their ETH. Also, because these protocols and most of their token liquidity are native to Ethereum main net, it can be exceptionally expensive to manually deposit to multiple protocols or buy multiple tokens off secondary markets in an effort to diversify your stake. Diversified Staked ETH (dsETH) addresses both of these pain points by indexing the most prominent liquid staking tokens and bundling them up into a single ERC20 token.

dsETH delivers value to customers by…

- enabling simple exposure to the top liquid staking tokens

- socializing gas costs associated with maintenance and rebalancing

- encouraging competition and decentralization in the liquid staking market

dsETH benefits the Index Coop by…

- diversifying our ETH product offerings

- expanding the broader category of yield products

- deploying our first Index-Protocol-based product

3.0 Overview

dsETH will be built on Index Protocol and contain Rocket Pool, Lido, and Stakewise liquid staking tokens. Lido’s stETH will be wrapped in order to accommodate its rebasing nature and Stakewise’s dual token model will be abstracted into a single set token so that staking rewards will accrue to a single ERC20. Flash Minting will also be enabled at launch, allowing users to deposit ETH or ERC20s and receive dsETH tokens in return.

3.1 Differentiation

Though there are many different liquid staking tokens in the DeFi ecosystem today, there are no on-chain offerings that index or emulate the same strategy as dsETH. This table presents the liquid staking tokens that will be present in dsETH and their respective yields:

| Token | Issuer | Protocol Fees | APR Net |

|---|---|---|---|

| stETH | Lido | 10% | 4.68% |

| rETH | RocketPool | 15% | 4.80% |

| sETH2 + rETH2 | Stakewise | 10% | 3.77% |

Source: Dune Analytics

As a result, the initial composition for dsETH will yield an estimated 4.24% APR after accounting for the streaming fee (0.25%). This is a simple projection, and it is worth noting that a variety of factors - percentage of ETH staked, network fees, fee burn - fundamentally affect the staking rate (thus yield is subject to change over time).

3.2 Example composition

dsETH will have the following composition at launch:

- Rocket Pool rETH: 43.9%

- Lido (w)stETH: 29.7%

- Stakewise wrapped sETH2: 26.4%

Staking and execution layer rewards will gradually accrue to the token’s value and be realized in the form of price appreciation.

3.3 Backtest results

Backtest calculations are shown for the period 13 March 2022 to present. The former is the earliest date for which complete price history is available for all constituents. The green plot shows the price history of dsETH in USD terms, the blue plot dsETH spot price in ETH terms, and the red plot dsETH “NAV” price in ETH terms. It is important to note that the dsETH “NAV” price (red) assumes 1:1 exchangeability between the underlying assets and ETH. The dsETH spot price in ETH terms (blue) can decrease due to decoupling between the underlying staked ETH tokens and ETH; an example would be the discounted exchange rate for stETH relative to ETH. Historical data on node operators were not available so we assumed a uniform allocation across the constituents.

You can also view backtest calculations here and here.

4.0 Size of Opportunity

There is $21.8B worth of ETH staked on the beacon chain today, and $7.7B of that is from liquid staking pools. ETH staked on the beacon chain has consistently risen since the contract went live in November 2020.

It is generally expected that the amount of ETH staked will increase over time, but using present values, if dsETH is able to capture 1% of the liquid staking market, that will amount to $77m in TVL for the product.

5.0 Market & Customer Research

5.1 Target Customers

dsETH is a relevant product for all customer types that the Coop currently serves: retail, DAO treasuries, and institutions. Because ETH is a core component of almost every crypto portfolio, all of these investor types stand to gain from a low-risk staking index like dsETH.

During DAO Treasury research, an ETH yield token was the most requested non-stablecoin product, and many treasuries today are seeking to deploy their ETH productively and earn a reasonable yield. Anecdotally, Rook DAO recently implemented a similar diversified staked ETH strategy to dsETH, though in a more manual fashion.

Regardless of customer type, this product will deliver a sustainable return on ETH!

5.2 User stories

- As a token holder, I want sustainable yield on my ETH

- As a token holder, I want diversified exposure to liquid staking tokens

- As a token holder, I want to distribute my stake across multiple protocols

- As a token holder, I want to support decentralized and permissionless staking protocols

- As a token holder, I want to support a balanced liquid staking market

5.3 Product economics

We predict monthly revenue of $5,208 and negligible rebalancing costs for a gross profit margin of effectively 100%. This is based on a $25M NAV, 0.25% streaming fee, and negligible rebalancing.

5.4 Product financial forecast

Financial forecast 2 of monthly streaming fee revenue assuming $25M max NAV, 1 month to half max NAV, 0.25% streaming fee, and no underlying appreciation. The rebalancing is very infrequent so the costs are effectively zero and the gross profit margin 100%.

6.0 Methodology

6.1 Initial Composition & Token Inclusion Criteria

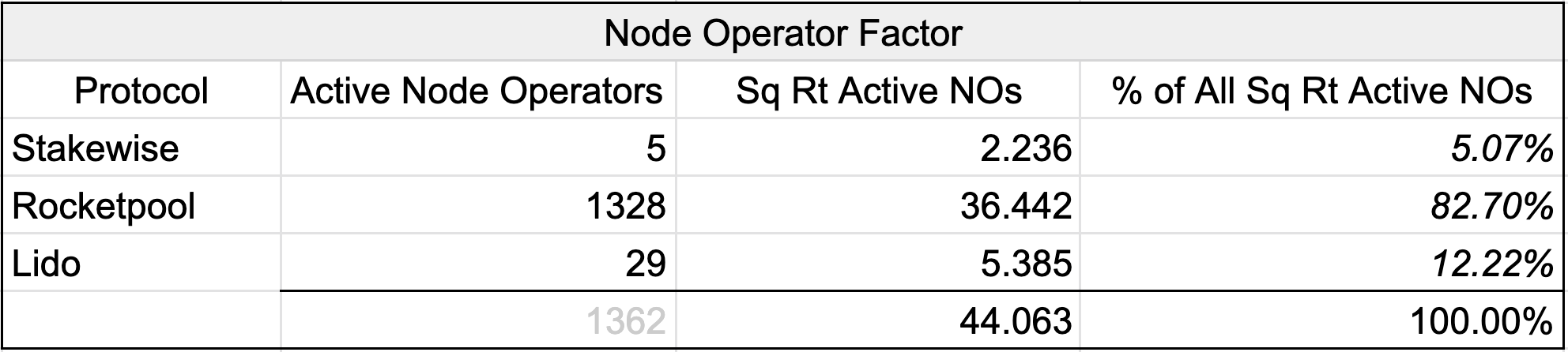

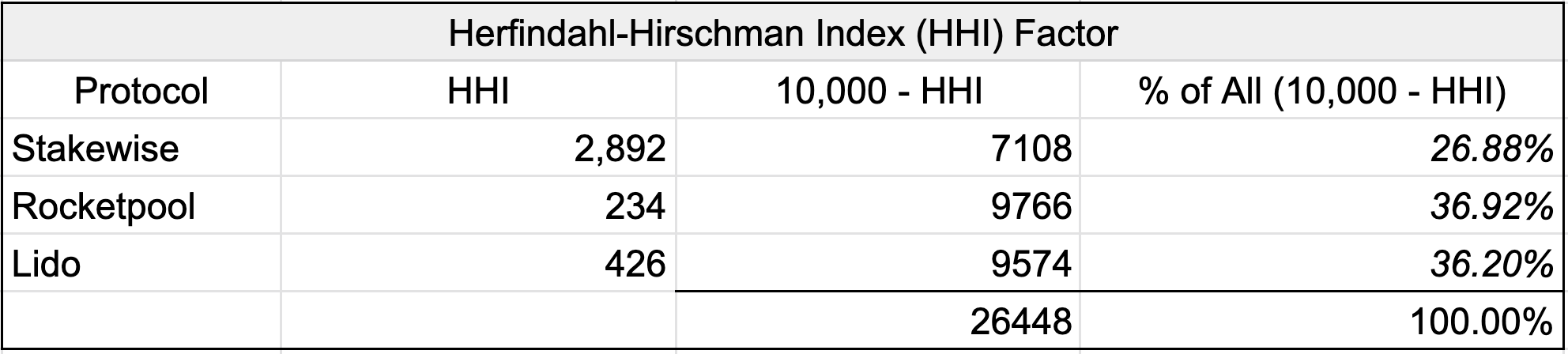

[values updated as of 12.22.22] The objective of the dsETH methodology is to give token holders diversified exposure to liquid staking tokens, with a weighting that favors decentralized liquid staking protocols as measured by the number of node operators as well as distribution of stake across node operators. To begin, constituents are equally weighted before adding a Node Operator Factor, which benefits staking protocols with more active node operators.

An HHI (or Herfindahl-Hirschman Index) Factor is then added, which measures the concentration of stake and broader competition amongst active node operators within each protocol.

After applying both of these factors, dsETH will have the resulting composition:

Token Inclusion Criteria:

- liquid staking tokens must be available on the Ethereum blockchain

- liquid staking tokens must have a minimum of 20,000 ETH in market cap

- liquid staking tokens must have a 30d Net APR that is not 10% below the mean Net APR for the largest liquid staking tokens

- staking protocols must be audited and reviewed by security professionals to determine that security best practices have been followed

- staking protocols must also be in operation long enough for the decentralized finance community to arrive at a consensus regarding its safety

- staking protocols must be open source

- staking protocols must have a bug bounty program

- no single client can account for two thirds (2/3) of a liquid staking protocol’s client distribution

Other liquid staking tokens that meet these criteria can be added to the index over time. No one liquid staking token can exceed 50% of the index, and the minimum allocation for a liquid staking token is 5%.

6.2 On-Chain liquidity analysis of underlying tokens

| Token | Largest DEX | Trade Depth @ 1% |

|---|---|---|

| sETH2 | Uniswap V3 | 14,614 ETH ($17.6m) |

| rETH2 | Uniswap V3 | 3,070 ETH ($3.7m) |

| rETH | Balancer V2 | 4,575 ETH ($4.6m) |

| wstETH | Balancer V2 | 177,000 ETH ($215.5m) |

6.3 Maintenance / Rebalancing frequency

Rebalancing will be performed semi-annually or every 6 months in an effort to minimize exposure to secondary market pricing for liquid staking tokens before staking redemptions are enabled by the Shanghai update. Rebalancing parameters may be revisited after the Shanghai update.

7.0 Costs

7.1 Cost to customer

Holders will pay a 0.25% streaming fee. There will be no mint fee and no redeem fee.

7.2 Cost transparency

NAV decay is an implicit cost associated with this strategy (though it is excluded from the effective yield communicated in this proposal). NAV decay due to impermanent loss is expected to be negligible due to infrequent rebalancing, but is possible if constituents do not have a 1:1 exchange rate with ETH during rebalance periods. Price impact related to rebalance trades will also contribute to NAV decay.

7.3 Fee split

The streaming fee will go 100% to Index Coop.

8.0 Meta / intrinsic productivity

Token holders stand to benefit fro

| Voter | Cast Power | Vote & Rationale |

|---|---|---|

0x6CD4...64443a | 271,488 | FOR |

Wintermute Governance | 197,955 | FOR |

0xce0D...46Adac | 120,455 | FOR |

0xB639...3a9623 | 112,922 | FOR |

0x0F7A...934BDb | 75,000 | FOR |

VOTE POWER

Proposal Status

- Thu December 22 2022, 10:23 pmVoting Period Starts

- Sun December 25 2022, 10:23 pmEnd Voting Period

Current Results

1-FOR

874,285.542

2-ABSTAIN

67.218